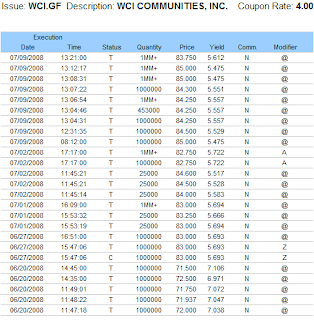

WCI Communities, the award winning builder of retirement and golf communities consisting of homes and condos in high rise towers mainly in Florida and the North East, wasn't really relaxing in the sun during the past year and a half. Finally though WCI is resting in peace, after repeated actions of trying to restructure its 4% convertible senior subordinated notes due 2023 that had a $125 million put date on August 4, 2008, which investors decided to redeem in full for cash. WCI did not have the liquidity available to pay off the notes, and if they did, it would have violated existing debt covenants using cash on hand to pay off those notes, so they tried to refinance them with secured notes paying 17.5%, giving it more security as well as shortening the expiration to 2012. They also sweetened the deal by providing a warrant to purchase 33 shares for each 1,000 principal amount. This transaction required that 95% of the 125 million be swapped. It's interesting that the convertible debt was being bid up about a month before the put date, they were pretty big sizes and could've been used to block the transaction or try to utilize the put at par realizing a nice cash profit. Bond activity information used from Finra.org.

And the funniest part of the story is there was a fake fax message sent to all of the media outlets in Florida that WCI received a $5.25/share bid to buy the company!

"WCI Communities said it was victimized by a phony press release Saturday that said the financially strapped luxury developer had received a buyout bid of $5.25 per share. As the buyout rumor circulated Monday morning, the company's stock shot up 37 cents per share, or 27 percent. WCI rushed out a press release denying the "false media reports," and the stock dropped back to its starting price of $1.37 per share. It closed at $1.39. WCI is best known in the Tampa Bay area for developing Sun City Center and the Westshore Yacht Club. As of late Monday, the company hadn't discovered the source of the fake news report, but suggested the U.S. Securities & Exchange Commission would look into whether someone was trying to pump up the stock to dump shares at a profit." Link

This all happening while S.A.C Capital is unloading millions of shares before the Aug 4Th put date, thousands of put contracts were bought sporadically during July at the lowest (2.50, 5.00) strikes, and 15 million shares were short. It's a conspiracy! Someone long needed some liquidity fast to get out, and the shorts were getting ready for the big BK!

The swap transaction ultimately failed and WCI filed for Chapter 11 bankruptcy. Here are quotes from the Chairman Carl Icahn, owner of 15% of the company..

“The company, with all diligence, has attempted to avoid a bankruptcy filing. However, the filing became necessary because of the recent failed effort to obtain financing and the recognition that the company’s entire $1.8 billion of debt may soon be in default. This was confirmed when certain holders of the company’s $125 million convertible notes informed the company that they rejected its exchange offer and instead insisted on being paid in cash in full on August 5, 2008.”

WCI went into bankruptcy cash flow positive with a $5.64 book value (Assets $2.13 Billion - 1.94 Liabilities), however banks were appraising the secured assets and some came in less than book value. From the 2Q press release:

"These lower than expected appraisal values could potentially trigger a mandatory repayment obligation in future periods. Thus far, we have received appraisals on assets totaling approximately $700 million of which aggregate appraisal values exceed 95% of book value, however, the ratio of appraised value to book value received to date may or may not represent the ratio of appraised value of remaining inventory." There was also commentary in the Naples News

It should be known that in 2007 WCI's previous board of directors turned down a $22 tender offer by Carl Icahn thinking they could get a better deal. This was a horrible idea because the housing industry was crumbling, especially in Florida, and now a year later the company is in Chapter 11 bankruptcy trading at .30 on the pink sheets.

In late 2006 and the beginning of 2007, Carl Icahn accumulated about 15% of the company and S.A.C Capital, High Bridge and Sandell Asset Management had just under 10% of the company trying to capitalize on a sale of the company. Carl Icahn and his affiliated companies then made a tender offer for WCI at $22/share on 3/23/07 if certain conditions were met (poison pill and Delaware law condition). Icahn's tender offer expired 2 months later because the company declined and did not agree with the conditions. In July WCI still couldn't come up with buyers for the company, and it was trading around $10/share and during this time I remember thousands of puts were traded at the 10.00 and 7.50 strike. It eventually hit $5 in the beginning of August.

Icahn was able to get the chairman role and get his nominees on the new board (including SAC and Sandell) at the August 30, 2007 meeting. Also at the beginning of September, 2007 WCI terminated the sales process because it received NO buy out offers. The previous board, headed by Don Ackerman, really screwed over shareholders who wanted out at the best price possible.

Carl Icahn's words from the SEC filing on 3/13/07.

"Carl Icahn concluded that "this tender offer will be in the best interests of all shareholders in that it would provide immediate liquidity at a premium for those shareholders who are concerned with the current housing industry downturn while also providing the opportunity for those shareholders who, like us, believe in the long-term prospects of the company to realize any potential upside."

WCI's reply's to Carl Icahn's offer from "WCI Rebuffs Icahn Buyout Bid" (TheStreet.com).

WCI said late Thursday that the $22-a-share offer is "highly conditional, opportunistic and inadequate from a financial point of view." The board instead plans to seek a sale on its own, and hired Goldman Sachs to help in the effort.

``WCI's Board of Directors believes that the Icahn tender offer is not in the best interests of all stockholders,'' said Chairman Don Ackerman. ``We reached this conclusion after carefully considering the tender offer price and terms, as well as the advice of our financial and legal advisors."

Carl Icahn's words from the SEC filing on 5/21/07

"Carl Icahn announced today that the any and all cash tender offer at $22.00 per share for shares of WCI Communities, Inc. expired at midnight, Friday, May 18, 2007, with none of the approximately 10.8 million shares tendered being purchased by his affiliates. This resulted from the failure by WCI to redeem the poison pill and meet the condition regarding Section 203 of the Delaware General Corporation Law. Mr. Icahn stated that he will have much more to say about this subject, but it is sufficient to point out that WCI prevented its stockholders who were desirous of achieving liquidity at a substantial premium from doing so. Mr. Icahn further stated, "I hope for the stockholders' sake that WCI has a bid for the Company better than $22.00 per share or else it was reprehensible to take away this opportunity from them. Should WCI fail to achieve such a sale price, we hope that stockholders will support our proxy fight to unseat the current Board of Directors."

In Conclusion:

Due to the beginning of the credit crisis and the distressed housing situation moving into the end of 2007 and 2008, WCI was able to stay alive for 9 months by amending important bank covenants, including the Debt/Tangible Net Worth ratio and EBITDA/Fixed Charges limit. WCI was lowering prices as much as 40% to unload as much inventory as they could to raise cash. Using the cash they could receive from their contract receivables, they were able to pay down 350 million of long term debt during the first 6 months of 2008 (1.92 to 1.58), however the net effect of the asset write downs didn't help out the NAV. They were also able to sell the Tuscany Reserve property for $65 million, however they realized a huge loss. Unfortunately for WCI it was horrible timing for asset sales to reduce debt obligations because land values were selling for distressed prices, and the high cancellation rates, lawsuits and daily operation expenses weren't helping the cash flow situation. The only thing that could've saved this company was a cash injection from Icahn, an overseas buyer utilizing the cheap dollar, or a private equity firm with a long term investment horizon. I don't think it was viable for Carl Icahn to inject 100s of millions of dollars, over his $120 million initial investment, to refinance the convertible debt as well as the other debt coming due. It's too bad because housing should be bottoming in 2009, and housing equities would reflect that before it actually occurs. With not enough cash coming in and cheap land appraisals, WCI had to reorganize to deal with their massive interest payment obligations.

0 comments:

Post a Comment