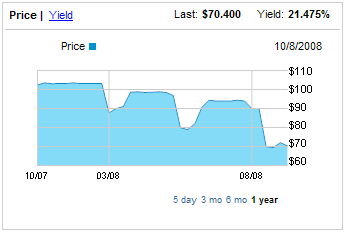

In early 2008, the sewage hit the fan when the auction rate market froze and banks refused to be the buyers of last resort which caused interest rates to double. On top of that, Moody's and S&P downgraded the County's insurance company FGIC that insured the bonds, which in turn forced investor liquidations and boosted rates even higher. And to finish it all off Moody's and S&P cut Jefferson County's debt rating to junk due to their debt service coverage issues. Eventually Jefferson County couldn't pay their interest payments and defaulted on billions of dollars now owed to swap obligees, and debt holders through insurers. Weren't those interest rate swaps supposed to hedge against interest rate risk? The swaps were not protecting against default or marketability (failed auction) risk which spiked up their interest costs. The swaps were protecting against floating market rate risk since the County refinanced into variable rate debt. In Feburary of 2008, floating market rates were actually moving lower while Jefferson County's interest rates were spiking, so the hedge worked against them. Below is a chart of one of the sewer bonds which is distressed yielding 21%. More information on this sewer bond can be found at finra.org. (Sources: Bond Buyer, Businessweek, Bloomberg, BusinessStandard).

As of 10/8/2008 (Last Sale) - Finra.org

It's also interesting that it looks like both the banks and the County are trying to hold off a bankruptcy court hearing for as long as they can, and from this article it looks like Jefferson County is trying to squeeze tax revenue from other sources.

October 13, 2008

"Jefferson County commissioners spar over sewer debt solutions

A Jefferson County commissioner in favor of bankruptcy said today that bringing an opposing sewer debt rescue plan to the state Legislature will draw gambling into the solution talks. Commissioner Jim Carns, who favors declaring Chapter 9 bankruptcy, said Commission President Bettye Fine Collins "better be careful" moving forward with a plan to get legislative approval for using excess education sales tax money toward reducing the $3.2 billion debt. "Because if it goes to the Legislature, gambling will be part of the scenario, in my opinion," Carns said. Carns comments followed a committee meeting earlier today and touched off the latest controversial exchange between commissioners at odds over solutions to county's sewer debt crisis." Source Al.com

Here's a 2 part video on BloombergTV interviewing Christopher Taylor, the former Executive Director of the Municipal Securities Rulemaking Board, about Jefferson County, AL.

This story shows that even municipalities are falling victim to the lax lending standards and risky derivatives originated in the early early 2000s. My next post will look at Municipal Bond Indexes and ETFs to watch.

0 comments:

Post a Comment