"Libor, set every morning in London, is what banks pay to borrow money from each other. That in turn determines prices for financial contracts valued at $393 trillion as of Dec. 31, 2007, or $60,000 for every person in the world, and helps set consumer interest rates on everything from home loans to credit cards.

Corporate bank loans are often linked to three-month Libor rates. Libor also affects interest costs on credit cards, student loans and adjustable-rate mortgages. From 2004 to 2006, more than half of the U.S. subprime mortgages at the root of the financial crisis, or those issued to the least creditworthy borrowers, had adjustable rates linked to Libor, said Guy Cecala, publisher of Inside Mortgage Finance in Bethesda, Maryland." Source: Bloomberg.com, 10/3/2008

Click For Larger Image, via Bloomberg Link

Click For Larger Image, via Bloomberg Link

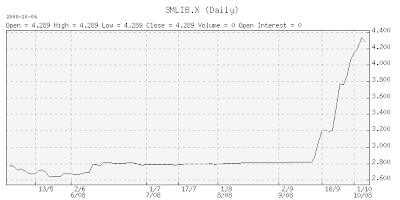

This rate is very important because it measures liquidity risk between banks. Because of so many bank failures recently in the U.S and Europe, banks were unwilling to shell out 3 month loans to other banks because of solvency risk. As a result 1 month and 3 Month LIBOR rates spiked, making it more expensive to borrow money. As stated in the description above, the 3 Month LIBOR rate is linked to corporate bank loans, as well as consumer loans including adjustable rate mortgages. Here's a recent chart of the 3 Month LIBOR rate and you can see it spiked recently due to the financial mess.

It's pretty crazy that 3 Month LIBOR increased 50% from 280 basis points (2.8%) in mid September to 420 basis points (4.2%) today. That is a dramatic increase, and since adjustable rate mortgages are tied to LIBOR, some home owners could see higher monthly payments which could squeeze household debt coverage. Plus heating costs are expected to increase by 15% this winter. Here's a quote from another Bloomberg article today, "Libor Rise to Boost Subprime ARM Defaults 10%, Citigroup Says".

"Oct. 7 (Bloomberg) -- Increases in benchmark London interbank offered rates may boost homeowner defaults on resetting adjustable-rate mortgages, contributing to a ``vicious cycle'' in the credit crunch, according to Citigroup Inc.

Among subprime loans, defaults may climb by 10 percent, analysts Rahul Parulekar, Udairam Bishnoi, Sumeet Kapur and Tanuj Garg wrote in a report yesterday. About $23.7 billion, or 87 percent, of the ARMs underlying bonds whose interest rates begin adjusting next month track Libor rates. Six-month dollar Libor has climbed to 4.02 percent, from 3 percent on Sept. 15.

The deepening of the credit crisis that started last year amid record defaults on subprime mortgages, contributing to $593 billion in writedowns and losses at banks worldwide, may end up causing more borrowers to fail to make their monthly payments. Libor rates, which track how much banks charge each other for loans, help set the cost of everything from credit cards to corporate loans."

If LIBOR doesn't see a relief correction, it would not only create more defaults, but kill consumer spending, and less spending means less profits, and less profits means more layoffs. There's the Fibonacci spiral again.....

On a more optimistic note, the Fed saw the situation and acted quickly. On Monday, since LIBOR was double the Fed's overnight target rate of 2%, the Fed announced a new commercial paper funding facility to provide 1-month and 3-month liquidity to relieve the pressure on short term borrowers. Hopefully this will take the risk premium out of LIBOR.

0 comments:

Post a Comment