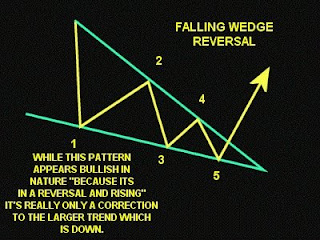

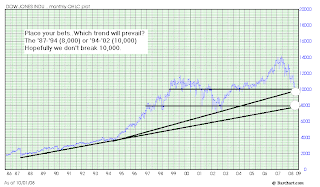

This economic bail out news is now a national joke on network tv and I'm starting to believe that negative sentiment right now is a coiled spring, and if the House passes this bill the $VIX will be sold off hard and the Dow could rally 1000 points, atleast in the short term. The indices are brushing up against the 15 year trend line and Warren Buffett is loading up on the best of breed. Of course the House needs to pass this bill in order to restore market confidence, or we will see, what Warren Buffet says, the "economic Pearl Harbor", and the rug under the US indices will be pulled.

What's surprises me is that the XLF and XHB have actually outperformed the SPY over the last 3 months, when IndyMac, Fannie, Freddie, Lehman, Merrill, AIG, WaMu, Wachovia all lost their lives. What else could seriously go wrong, besides the economy spiraling into a black hole. The XLF was up 9.92% and the XHB was up 27.8% on the SPY during the last 3 months! How crazy is that?? Shouldn't hedge funds be making those returns on the S&P and not sector index funds?

SPY vs. XHB & XLF 3 Month Chart (Source: Bigcharts.com)

Looking specifically at the XLF, it needs to clear above the $20 support level with strength to catch a major bid, and it needs to break above the downward trend. Plus you can see two capitulated lows on those volume spikes (between $15-20). That could in fact be a double bottom but it seriously depends on this bail out, which will unfreeze the banks and bring liquidity back to main street. If the bailout fails again confidence will not be restored and we'll probably see another volume spike to the downside.

XLF 4 Year Chart (Source: Bigcharts.com)

The XHB has been in the $15-25 range since last August. It hit all time lows ($15) this July, and since rallied to $20 even during the September mortgage/bank massacre. It looks like there's a floor between $15-20, and again if the bill passes it will provide liquidity to the mortgage market as the tax payers scoop up the worthless mortgage paper from the banks, which would allow builders to work off existing inventory and raise cash.

XHB 4 Year Chart (Source: Bigcharts.com)

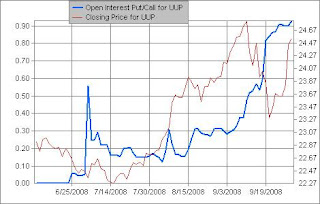

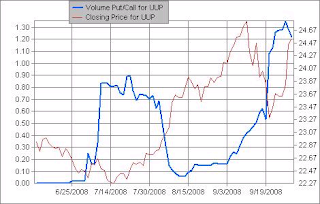

These last charts show investor sentiment indicators of XLF. The chart below shows XLF Implied Volatility spiking recently. It's implying a big move ahead and I'm pretty sure volatility is being bid up in anticipation of the House vote. Either way once the news is out IV will be sold and the XLF will move in the appropriate direction. The XLF put/call open interest ratio is at 0.82 which is bullish bias and you can see the open interest configuration below with the large chunks of out of the money calls open. Plus short interest has been breaking down since June. So it will be interesting to see what happens here, and hope for the best.

XLF Schaeffers Volatility Index (Source: Schaeffersresearch.com) XLF Put/Call Open Interest Ratio (Source: Schaeffersresearch.com)

XLF Put/Call Open Interest Ratio (Source: Schaeffersresearch.com) Go to Schaeffersresearch.com for great option data and charts.

Go to Schaeffersresearch.com for great option data and charts.

Click For Larger Image, via Bloomberg Link

Click For Larger Image, via Bloomberg Link

Source: Time Magazine Cover 10/13/08

Source: Time Magazine Cover 10/13/08